Graphing Digital Assets

Month in Review — March 2025

Bitcoin as a Hedge Against Macro Risk?

Both traditional and digital asset markets experienced significant downturns in March, leading some investors to revisit bitcoin’s role in diversified portfolios. The S&P 500 Total Return Index dropped 5.63% during the month and had its worst quarterly showing in nearly three years, while bitcoin declined 2.16% in March. Despite this relative outperformance, bitcoin’s trajectory will likely hinge on how convincingly it can assert its role as a store of value and inflation hedge. For now, it continues to trade like a high-beta risk asset, driven more by the behavior of investors than by underlying fundamentals.

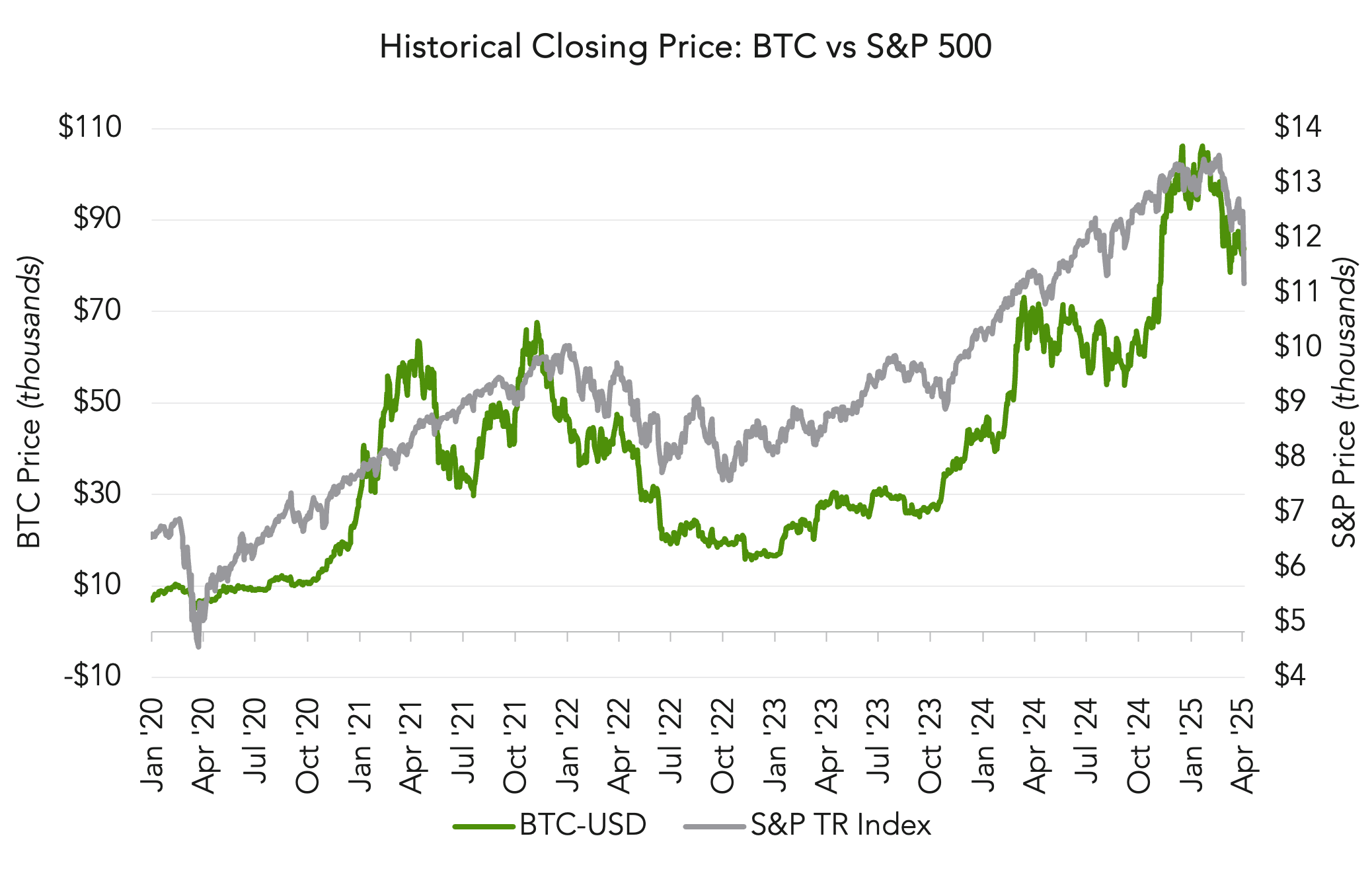

A price comparison (Figure 1) reveals episodes of alignment and divergence over the past five years. A 30-day rolling correlation chart further illustrates this (Figure 2*): both bitcoin and the S&P 500 fell during broad macro stress—such as the COVID crash and the 2022 rate hike cycle—when correlation spiked. However, correlation consistently faded during periods of stabilizing monetary policy and crypto-native enthusiasm, including the post-COVID liquidity boom, the DeFi-led rally following the 2023 banking turmoil, and bitcoin’s ETF-driven surge in late 2023 and early 2025. This episodic behavior underscores bitcoin’s potential to break from traditional market dynamics under the right conditions.

This pattern reinforces that bitcoin’s correlation to traditional markets has historically been episodic—not structurally high or low, but reactive to regime shifts in liquidity, policy, and positioning. While equities are driven by earnings and economic growth, bitcoin’s valuation is more reflective of capital flows, monetary conditions, and its evolving role as a store of value.

The current macro environment has reignited hopes within the bitcoin community of a long-awaited “decoupling moment”—a clean divergence where bitcoin rises despite weakness in broader markets. For many, this would mark bitcoin’s arrival as a true hedge against inflation and macro instability. So far, however, it has shown only flashes of independence without fully sustaining them. The question is not whether bitcoin will decouple—but under what conditions, and for how long.

While short-term volatility remains likely, with greater regulatory clarity, broader adoption, and mounting monetary instability, bitcoin may emerge not just as a speculative asset, but as a resilient alternative in a shifting global landscape.

Figure 1

Figure 2

*Source for S&P TR Index: Yahoo Finance; source for BTC price: CoinmarketCap. As of April 6, 2025, close.

Figure 2 Legend:

(1) Q1 2020: Leading up to the COVID crash, correlation spikes as BTC trades in line with risk assets amid broad selloff.

(2) Nov 2020: In the post-COVID liquidity boom, correlation fluctuates; BTC decouples during a QE-fueled rally.

(3) Mar 2022: Fed tightening begins and correlation remains elevated as macro forces dominate.

(4) Mar 2023: Post-Silicon Valley Bank fallout, correlation drops as BTC rallies on DeFi tailwinds and systemic banking fears, while equities stay rangebound.

(5) Q4 2023: In an ETF anticipation rally, correlation declines as BTC rises on crypto-native momentum, while equities remain cautious.

(6) Aug 2024: Risk-on resurgence causes correlation to increase as both BTC and equities rally on Fed pivot hopes, slowing inflation, and political tailwinds.

(7) Q1 2025: BTC-led rally resumes and correlation drops sharply as BTC extends a crypto-native surge while equities pause on mixed macro signals.

How Digital Assets Stack Up

Over the past several market cycles, since January 2018, the performance of major asset classes reveals a wide dispersion of outcomes and highlights the distinct outperformance of digital assets relative to more traditional investments.

Bitcoin stands out with cumulative returns exceeding 483% through March 31, 2025, far outpacing equities, private equity, real estate, and fixed income. However, this outperformance comes with substantial volatility, positioning it at the extreme end of the risk-return spectrum. For long-term holders, the trade-off has been rewarded, but it underscores the importance of understanding how an asset’s return potential and risk characteristics interact with the broader portfolio.

Private equity and equities delivered solid gains with considerably lower volatility. Real estate and bonds, by contrast, offered the most stability, but also the lowest cumulative returns—reflecting their roles as income-generating and defensive allocations.

What stands out in this period is the performance of market-neutral digital asset hedge funds relative to “traditional alternatives”. This strategy not only delivered more consistent returns than private equity and real estate, but did so with lower volatility. On a risk-adjusted basis, it falls in the most desirable northwest quadrant of the risk-return matrix—an outcome rarely achieved by alternatives that typically rely on illiquidity or leverage to enhance returns.

While data for private equity and real estate is available only through 2024, updated figures for actively traded asset classes provide further context. From January 1, 2018 through March 31, 2025:

Bitcoin delivered an annualized return of 27.5% with volatility of 71.3%

S&P 500 returned 12.7% annually with 17.1% volatility

Bloomberg U.S. Aggregate Bond Index returned -1.4% annually with 5.7% volatility.

This performance reinforces the broad dispersion of risk-return profiles across asset classes.

In an environment marked by macro uncertainty and elevated asset correlations, the diversification benefits of low-volatility, liquid alternatives becomes particularly relevant. Market-neutral digital asset strategies in particular are well-positioned to complement traditional alternatives, offering new ways to enhance portfolio resilience without dramatically increasing risk.

Figure 3

Figure 4

Past performance is not indicative of future results. Data as of December 31, 2024, unless noted otherwise. Source for Bitcoin data: Coinbase. Market-Neutral Digital Asset Funds as represented by Galaxy VisionTrack Market Neutral Index; US Private Equity as represented by Cambridge Associates US Private Equity Index (as of September 30, 2024, most recent available); US Equities as represented by S&P500 TR Index; Real Estate as represented by NCREIF NPI Property Index; Fixed Income as represented by iShares Core US Aggregate Bond ETF.

Bitcoin on the Balance Sheet

Bitcoin’s role as a corporate strategic asset continued to gain momentum. In March, GameStop’s announcement to add $1.5 billion of bitcoin to its balance sheet underscored the growing trend of high-profile companies integrating bitcoin into their treasury strategy.

Amid this growing corporate adoption, two distinct approaches are emerging—one measured and conservative, the other more aggressive.

Bitcoin as a Treasury Reserve Asset

A growing number of companies are allocating a portion of their capital to bitcoin as a hedge against inflation and fiat debasement. This approach mirrors traditional reserve strategies, with firms integrating bitcoin alongside cash and gold to enhance portfolio resilience.

Figure 5 highlights bitcoin holdings among the top 10 publicly traded companies with significant allocations, including Strategy (formerly MicroStrategy), Tesla, and Block. These firms hold bitcoin alongside traditional reserves, positioning it as a core asset, and typically rely on custodians or spot ETFs for exposure.

Aggressive Accumulation Using Debt and Equity

Companies taking this bolder approach raise capital—via convertible debt or equity—specifically to purchase bitcoin. These firms aim to proactively increase their bitcoin reserves to maximize exposure and growth potential.

Strategy (MSTR) pioneered this method, turning its bitcoin holdings into a central part of its business strategy and introducing “bitcoin per share” (BPS) as a key metric. Figure 6 illustrates Strategy’s bitcoin accumulation over time through convertible debt, with BPS rising as shares per bitcoin decline. Samara Alpha’s parent company, Samara Asset Group, as well as Metaplanet and GameStop, have followed suit, using traditional finance tools to leverage and scale their bitcoin positions.

As institutional participation deepens and bitcoin continues to gain legitimacy as a treasury asset, major firms like Apple, Microsoft, and Amazon will likely face mounting pressure to integrate bitcoin into their treasury strategies. Regulatory clarity and political momentum are accelerating this shift—most notably with Trump’s March announcement creating a U.S. Strategic Bitcoin Reserve, underscoring bitcoin’s rising geopolitical and macroeconomic significance.

Figure 5

Source: Bitcoin holdings by public companies from CoinGecko as of March 31, 2025.

Figure 6

Source: SaylorCharts as of March 31, 2025.