Spot Bitcoin ETFs: A Paradigm Shift

A deep dive into the implications of the approval of U.S. spot bitcoin ETFs by the SEC, particularly for institutional investors.

Jan 16, 2024The landmark approval of spot bitcoin exchange-traded funds (ETFs) in the U.S. on January 10, 2024, marks a significant milestone for the cryptocurrency industry. This breakthrough concludes a decade-long journey, overcoming prior rejections by the U.S. Securities and Exchange Commission. As an institutional digital asset manager, to us, the approval signals a paradigm shift in institutional adoption that includes regulatory validation of bitcoin as a new asset class, as well as enriched product innovation and cross-asset investments.

Spot bitcoin ETF trading began the day after its approval, immediately drawing considerable capital, with BlackRock and Fidelity emerging as market leaders. While some analysts project the approved ETFs to attract \$50 billion in assets within two years, we have a more conservative view of \$13 to \$18 billion in net inflows. Beyond growth projections, we explore broader implications, suggesting these investment products can overcome historical challenges faced by traditional financial institutions, as well as reshape cryptocurrency market structures and valuations.

Exhibit 1: Approved Spot Bitcoin ETFs

Sources: Samara Alpha Management, Bloomberg, SEC Filings as of January 12, 2024.

*Data not available at time of publishing.

Increased Accessibility to Cryptocurrency Via Traditional Investment Vehicles

Historically, navigating direct exposure to cryptocurrencies has had substantial hurdles. In recent years, however, exchange-traded products (ETPs) have made it simpler for investors to gain exposure to cryptocurrencies, alleviating complexities that have acted as a barrier to entry. In Europe, the cryptocurrency ETP market has grown to 166 listed products in January 2024 since 2014. In North America, Canada has led the way in crypto ETPs, with Purpose Investments launching the first spot bitcoin ETF in 2021 and reaching C$1 billion within its first month. Grayscale's Bitcoin Investment Trust (GBTC) has allowed investors to acquire shares in an OTC-traded fund with bitcoin as the underlying asset since 2013.

The approval of U.S. spot bitcoin ETFs plays a crucial role in broadening institutional adoption and legitimizing bitcoin as a viable asset class. As traditional financial institutions gain exposure through ETFs, they become more acquainted with bitcoin's functioning, potential, and risk-reward dynamics, leading to enhanced diversification strategies. This growing familiarity triggers a virtuous cycle, validating bitcoin and other cryptocurrencies as legitimate investment avenues within the broader financial landscape. Despite facing regulatory uncertainties, the U.S. market holds immense significance for the maturation of the cryptocurrency capital market.

An Arduous Journey

The approval of U.S. spot bitcoin ETFs follows an arduous 10-year journey, having begun with Winklevoss Bitcoin Trust, the first spot bitcoin ETF application in 2013.

Three key developments collectively influenced the regulatory landscape leading to the approval of spot bitcoin ETFs in the U.S., reflecting a dynamic interaction between regulatory guidance, industry applications, and legal challenges.

1. Gensler’s Guidance

On August 3, 2021, SEC Chairman Gary Gensler addressed the Aspen Security Forum in his "Remarks Before the Aspen Security Forum," paving the way for bitcoin ETFs. His speech lit up the race among traditional asset managers, notably BlackRock and Fidelity, towards filing cryptocurrency ETFs under the Investment Company Act of 1940 (40 Act). He pointed out that the 40 Act, in conjunction with other federal securities laws, provides significant investor protections. He also highlighted the importance of proper custody arrangements in protecting investors against theft, noting that the SEC will focus on “regulatory protections in this area.”

2. BlackRock’s Filing

On June 15, 2023, BlackRock filed an application with the SEC to launch a spot bitcoin ETF, strategically choosing Coinbase as a custodian and entering a surveillance-sharing agreement with Nasdaq. This marked a significant development for U.S. spot bitcoin ETFs, given Blackrock’s recognized position as a reputable traditional asset manager. The involvement of a major player like BlackRock generated optimism within the digital asset market as it presented the potential for a departure from the historical trend of denying such filings. The company's close ties with U.S. regulators and politicians suggested a potential impact on mitigating the prevailing regulatory challenges facing the crypto industry.

BlackRock's extensive track record of ETF filings (non-crypto), with an approval rate of 575 out of 576, added a positive dimension to the outlook for approval. The decision to pursue this filing indicates BlackRock's confidence in the long-term strength of bitcoin and the anticipation of substantial inflows.

3. Grayscale vs. SEC

Grayscale’s legal victory in 2023 against the SEC to file for conversion of its bitcoin trust into an ETF was key in the eventual approval of spot bitcoin ETFs in the United States. Grayscale applied to convert its flagship Grayscale Bitcoin Trust into an ETF in October 2021. This trust, approved by the SEC in 2015 and currently holding more than \$28 billion in bitcoin assets, had long aimed to transition into an ETF. Although the SEC had approved bitcoin futures ETFs in October 2021, it expressed concerns about spot funds, citing susceptibility to manipulation in largely unmonitored crypto markets, thereby rejecting Grayscale’s application.

In August 2023, a federal appeals court challenged the SEC's rejection of Grayscale's ETF conversion application. Judge Neomi Rao, in a ruling considered pivotal for the cryptocurrency industry, deemed the SEC's decision "arbitrary and capricious" for failing to justify its disparate treatment of similar products.

This legal development had placed the regulatory body at a crossroads, paving the way for the approval of spot bitcoin ETFs. Chairman Gensler was the tiebreaker of the votes, noting in his statement, “I feel the most sustainable path forward is to approve the listing and trading of these spot bitcoin ETP shares.”

Limitations of the Current Version of Spot Bitcoin ETFs

Spot bitcoin ETFs currently lack the operational efficiency that investors typically associate with other ETFs. The widespread popularity of ETFs stems from their cost-effectiveness, facilitated by in-kind creations and redemptions that enable portfolio managers to minimize trading activities and circumvent transaction costs. However, in the current version of spot bitcoin ETFs, creations and redemptions are cash-based.

In other words, spot bitcoin ETFs do not enjoy the advantages of in-kind creations or redemptions. The SEC has exclusively approved cash-based creations and redemptions for these ETFs, obliging them to bear the expenses associated with purchasing and selling bitcoin when ETF shares are generated or redeemed. The issuer must transfer the stored bitcoin and immediately sell it to provide cash, involving one custodian for cash or USD and another for bitcoin.

The absence of in-kind transactions in spot bitcoin ETFs raises concerns about potential trading costs that could impact the overall performance of these ETFs. The precise magnitude of these costs remains uncertain, but they encompass transaction expenses, bid-ask spread crossing fees, and market-impact costs. In the current competitive landscape, issuers possessing greater resources and expertise in capital markets have a strategic advantage to dominate this market.

First Impressions

In the first two days of trading, the net flow of capital into the approved spot bitcoin ETFs, excluding GBTC, amounted to an impressive \$1.4 billion. After deducting GBTC’s outflow, the net inflow for the initial two days is estimated at \$819 million. This surpassed the first two days of the first U.S. gold ETF (GLD) which reached \$709 million. Given the two assets’ shared properties (e.g., limited supply, decentralized nature, potential store of value) and the steep rise of the price of gold in the years following the launch of GLD, this meaningful comparison has implications for BTC price in the years to come.

What’s Behind GBTC’s Outflows?

Amid projections for the newly approved ETFs to attract $50 billion in assets within two years, in its first two days of trading, GBTC experienced a net outflow of \$579 million. Taking into consideration GBTC profit-taking and fees, we estimate spot bitcoin ETFs reaching between \$13 and \$18 billion in net inflows.

Profit-taking speculators are expected to capitalize on profits from the sale of discounted GBTC shares they acquired on the secondary market over the past year, having purchased the shares in anticipation that the discount to Net Asset Value will be eliminated upon conversion to an ETF. As a result, we estimate total outflow from GBTC will amount to more than \$3 billion of these sales.

Given Grayscale's relatively high fee of 150 basis points, an additional \$5 billion to \$10 billion could swiftly exit GBTC as investors migrate towards more cost-effective spot bitcoin ETFs. The potential loss of GBTC's status as the largest bitcoin fund globally weakens its liquidity profile, triggering further outflows.

Trading Trends

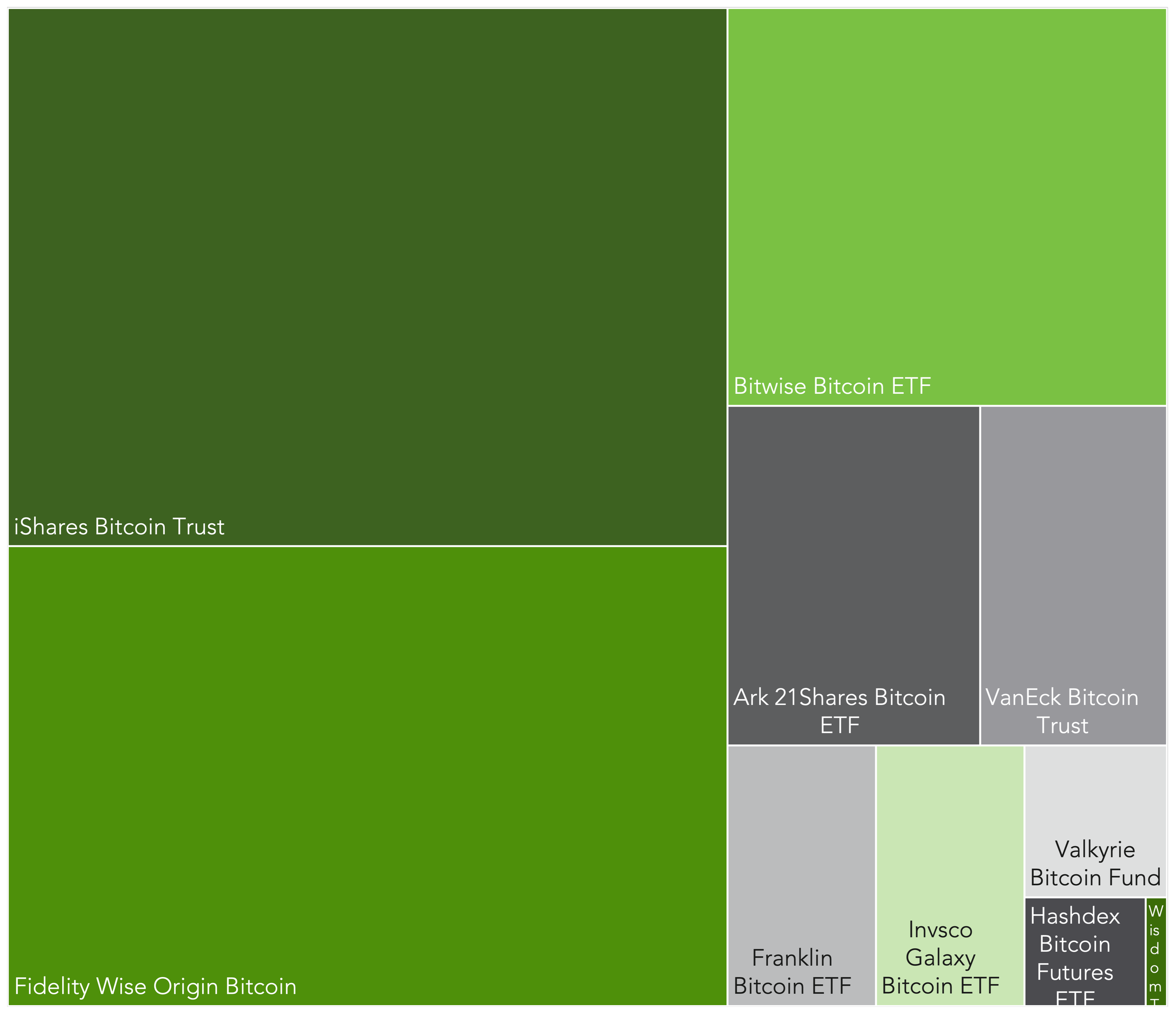

Spot bitcoin ETF initial trading day statistics suggest that BlackRock and Fidelity could lead in growing assets under management, given their initial market share (Exhibit 2) as well as their institutional and retail distribution networks. The impact of strong retail demand for U.S. spot bitcoin ETFs is expected to fuel institutional flows after a record first trading day. More than 700,000 trades were made with a turnover of just under \$5 billion, surpassing the number of shares traded on equity markets SPDR S&P 500 (SPY US) and Invesco QQQ (QQQ US) on that same day.

Exhibit 2: Market Capitalization of Spot Bitcoin ETFs (Ex-Grayscale) as of January 12, 2024

Sources: Samara Alpha Management and Bloomberg.

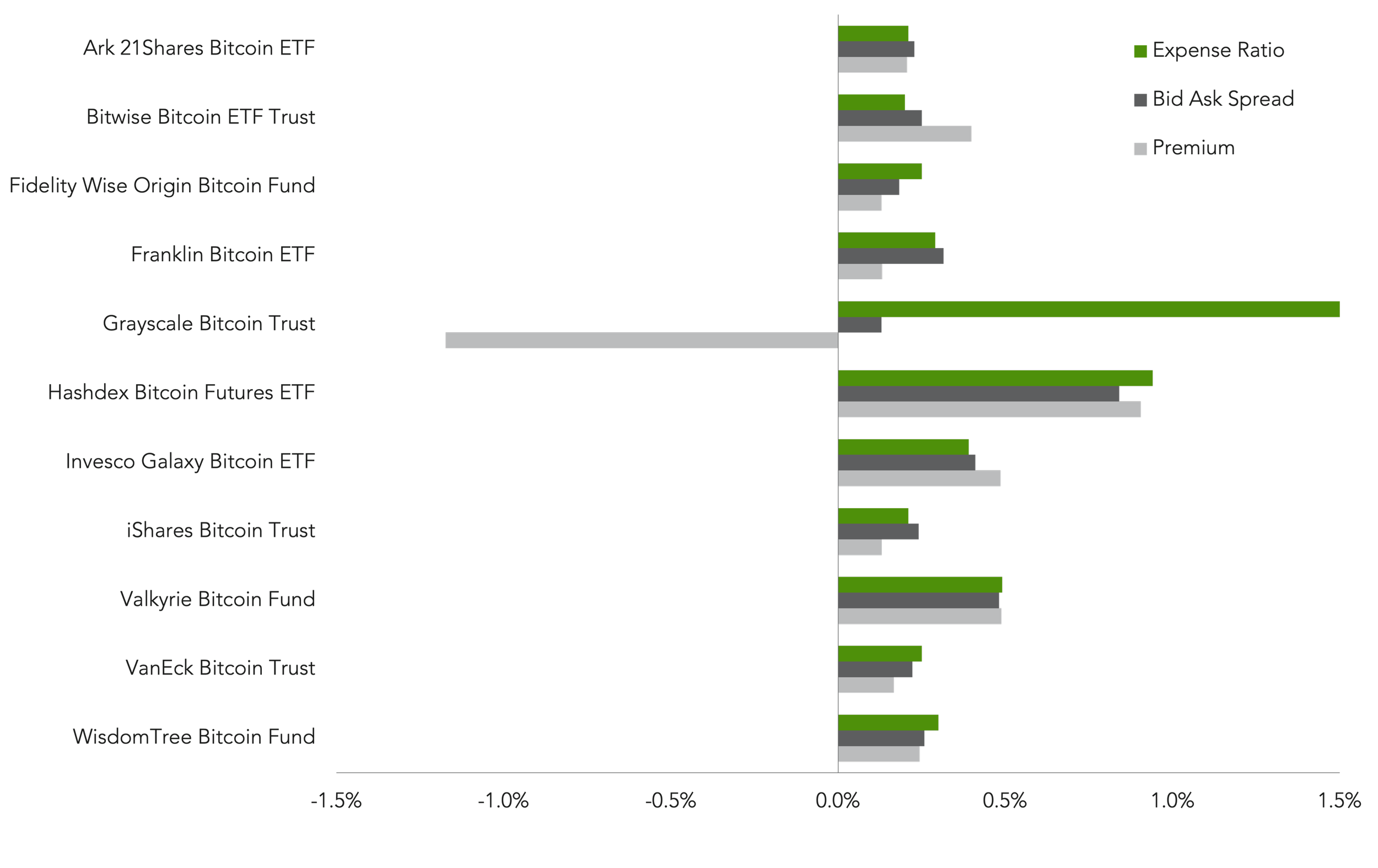

In the first week of spot bitcoin ETF trading, several noteworthy trends have emerged. Exhibit 3 shows that all the ETFs traded at a slight premium, ranging from 13 to 49 basis points, except Grayscale, which experienced a 1.17% discount due to its higher fees. Hashdex’s DEFI also stands out as an exception, maintaining a higher premium as its strategy is still rooted in futures rather than spot trading. Bid-ask spreads generally remained below 25 basis points, with Grayscale exhibiting the tightest spread at 13 basis points, reflecting its dominant liquidity before the transition to a spot ETF.

Exhibit 3: Spot Bitcoin ETFs and Costs

Sources: Samara Alpha Management, Bloomberg, SEC Filings as of January 12, 2024.

The SEC’s simultaneous approval of multiple filings has ignited intense fee competition among issuers, presenting a favorable scenario for investors. Spot bitcoin ETFs have significantly undercut the expense ratio imposed by existing crypto funds. Grayscale trusts, for instance, currently levy fees ranging from 2% to 3% on NAV, while the largest bitcoin futures ETF charges 0.95%.

Fees are expected to play a pivotal role in distinguishing the total returns of spot bitcoin ETFs. As seen in Exhibit 3, Bitwise’s ETF stands out with the lowest ongoing fee of 0.20%. However, fees on ETFs offered by ARK, Fidelity, VanEck, and Blackrock closely align, falling within 5 basis points of Bitwise. Issuers have also employed fee waivers to attract assets, with six of the bitcoin ETFs launching with a 0.00% fee. Grayscale, however, deviates from this trend with a proposed fee of 1.50%.

Impact of Liquidity

Liquidity costs can be dissected into two components:

Crossing the bid-ask spread: Traders incur a cost each time they buy at the offer or sell at the bid. The tighter the bid-ask spread the more efficient the trading experience.

Depth of liquidity: Investors seek sufficient shares near the current price for buying or selling, ensuring optimal prices during the execution of large trades. Tighter bid-ask spreads indicate deeper liquidity, implying a higher availability of shares to buy or sell near the current price.

Exhibit 4: Direct Bitcoin Investment Bid-Ask Spread

Source: Kaiko as of January 14, 2024

Exhibit 4 illustrates the liquidity of spot bitcoin ETFs within the context of spot bitcoin liquidity from the cryptocurrency exchanges. A narrower bid-ask spread indicates higher liquidity. Kaiko calculates this spread based on raw order book snapshots collected twice per minute. They then compute the average spread over one hour, resulting in a 24-hour moving average of the bid-ask spread. Exhibits 3 and 4 demonstrate that the bid-ask spread for direct investment into bitcoin is considerably tighter than that of spot bitcoin ETFs. This difference reflects inherent costs associated with the ETF wrappers, suggesting that retail customers incur a premium to access bitcoin through ETFs. Anticipating growth of the spot bitcoin ETFs and increased competition among market makers, the bid-ask spread is likely to compress over time.

While the bid-ask spread is expected to tighten, it is unlikely to reach the same levels as those on crypto exchanges. Institutional participants, such as market makers, authorized participants (APs), and professional arbitrageurs, will continue to profit from ETFs order flow. This dynamic will generate significant interest among institutional investors in the evolving landscape of spot bitcoin ETFs.

A Closer Examination of Costs

Spot bitcoin ETFs have notably enhanced the accessibility and exposure of retail investors to bitcoin. Nevertheless, their cost-effectiveness is not universally optimal. Exhibit 5 delineates critical expenses associated with spot bitcoin ETFs and direct bitcoin investments, fees that are ultimately passed on to investors.

Exhibit 5: Itemized Key Costs as of January 12, 2024

Sources: Samara Alpha Management, Bloomberg, and SEC Filings.

Knowing what these costs are enables us to understand their impact on an investment.

Premium / Discount: When the market price of an ETF is higher than its net asset value (NAV), it is trading at a premium. Conversely, if the market price is lower than the NAV, it is trading at a discount.

Creation Fees: Fees associated with the creation of new shares of an ETF. APs can create new shares by settling in cash with the ETF issuer. Creation fees cover the costs involved in this process.

Bid-Ask Spreads: The bid price is the highest price a buyer is willing to pay for a security, while the ask price is the lowest price a seller is willing to accept. The bid-ask spread is the difference between these two prices.

Expense Ratio: A measure of the annual operating expenses of an investment, expressed as a percentage of its total assets. It includes management fees, administrative costs, and other operational expenses.

Network Gas Fees: Commonly associated with blockchain networks like Bitcoin, gas fees are the costs associated with processing and validating transactions. These fees are paid in cryptocurrency and can vary based on network congestion and transaction complexity.

Broker and Exchange Fees: Fees charged by brokerage firms and exchanges for executing and facilitating trades. Broker fees may include commissions on trades, while exchange fees cover the costs of using the trading platform.

Custody Fees: Charges imposed by financial institutions for holding and safeguarding a client's financial assets.

The choice between a spot bitcoin ETF and direct ownership of bitcoin on a cryptocurrency exchange involves a trade-off between costs, control, convenience, and other factors. Investors with varying objectives may opt for different approaches based on their priorities. Active traders, who prefer to have direct ownership and control over their cryptocurrency holdings, manage their own portfolios and execute trades on exchanges. Using a cryptocurrency exchange allows them to manage their private keys and have immediate access to their assets. Conversely, other investors may prefer a spot bitcoin ETF, reducing the complexities of direct spot bitcoin investing with the added benefit of regulatory oversight in traditional brokerage accounts.

Implications of Spot Bitcoin ETFs

Spot bitcoin ETFs signify a pivotal shift in cryptocurrency market accessibility, alleviating some barriers to entry. Challenges related to navigating exchanges, establishing and maintaining electronic wallets, and managing blockchain risks have previously deterred institutional involvement, especially amid regulatory uncertainty. A spot bitcoin ETF addresses these issues by enabling investors to access bitcoin without direct ownership, entrusting ETF issuers to manage bitcoin exposure.

This approach, while deviating from bitcoin's core principle of self-custody, aligns with traditional investors’ interests, who prioritize compliance and risk reduction. The use of reputable custody providers further makes spot bitcoin ETFs more appealing to institutional investors seeking secure entry points into digital assets.

The introduction of spot bitcoin ETFs impacts liquidity, stability, and cost dynamics in the cryptocurrency market. Some potential benefits include:

Enhanced accessibility for a broader range of investors, potentially attracting significant institutional capital.

Setting a precedent, encouraging the launch of similar spot ETFs globally, as well as additional crypto financial products within traditional spaces, such as listed options.

Migrating cryptocurrency trading to equity markets over time, given the ease of accessibility and greater transparency.

Increasing liquidity, fostering a more stable price environment, and reducing extreme volatility within crypto markets.

Spot bitcoin ETFs are perceived as both cost-effective, owing to their low fees, and safer due to enhanced regulatory oversight. Assuming the migration of retail investors from various crypto exchanges and traditional brokers to these newly established spot bitcoin ETFs, we estimate the potential inflows from these channels, including future-based ETFs, to reach \$16 to \$20 billion, with net flows of \$13 to \$18 billion.

Illuminating the Road Ahead

The interconnected effects on liquidity, stability, and cost dynamics position spot bitcoin ETFs as a driving force capable of reshaping market structure, enhancing accessibility, and influencing cryptocurrency valuations.

The approval of spot bitcoin ETFs marks a significant milestone for the cryptocurrency industry, paving the way for institutional adoption and legitimization. Despite the initial success, challenges and risks associated with operational efficiency, diverse APs, and potential disruptions need ongoing attention, as with any asset class. The industry anticipates substantial growth with broader implications for the overall cryptocurrency market.